Using Claude Fable 5 to Analyze My Investment Portfolio

Anthropic just re-released its most capable model. I used it to analyze my own portfolio, and the results were a mix of useful and frustrating

I spent a few days last week trying to get Anthropic’s best model to analyze my portfolio. Unfortunately, it kept handing me off to a weaker one instead.

Claude Fable 5 is the new top of Anthropic’s lineup. It ranked highest on Hebbia’s financial-reasoning benchmark. IMC, a trading firm, noted it outperformed all their internal trading tests. It went live in June, got pulled offline three days later by U.S. export-control rules, and came back online last week.

Fable checks each request for risks, like cybersecurity and biology. If something raises a flag, it passes the session to Opus, a less powerful model. Anthropic says that happens in under 5% of sessions. Mine ran closer to half, sometimes on a prompt that had worked minutes earlier in another window. Anthropic confirmed that a portfolio review is allowed for Fable. I still don’t know what triggered this.

To start, I loaded a CSV of my stock and ETF holdings and gave Fable my age, filing status, net worth, income, and goals.

Generic advice isn’t advice

Be cautious with investment advice from anyone who doesn’t understand your financial situation. Their guidance may not be right for you. There’s no perfect investment. There are only those that fit your risk tolerance, time horizon, and goals better or worse. Advice from someone who doesn’t know your situation is close to worthless.

So before Fable analyzed anything, I had it quiz me to determine my risk tolerance. What people say they’ll do in a crash and what they actually did in the last one are usually different answers.

Fable’s quiz focused on behavior more than self-report. It asked what I did the last time the market dropped 40%. It also wanted to know why I’m still holding the bond funds. It asked which would hurt more: a position going to zero or missing a stock on my watchlist that tripled. Then it checked my answers against my cost basis to see whether I’d held through the lows I claimed I’d held through. It graded my trading history instead of my story about myself.

Checking the holdings against the goal

Once it had a read on my risk tolerance, Fable went through the holdings against my stated goals. It marked my bond and commodity allocation as too high for my goals. It also urged me to sell the positions that were too small to matter.

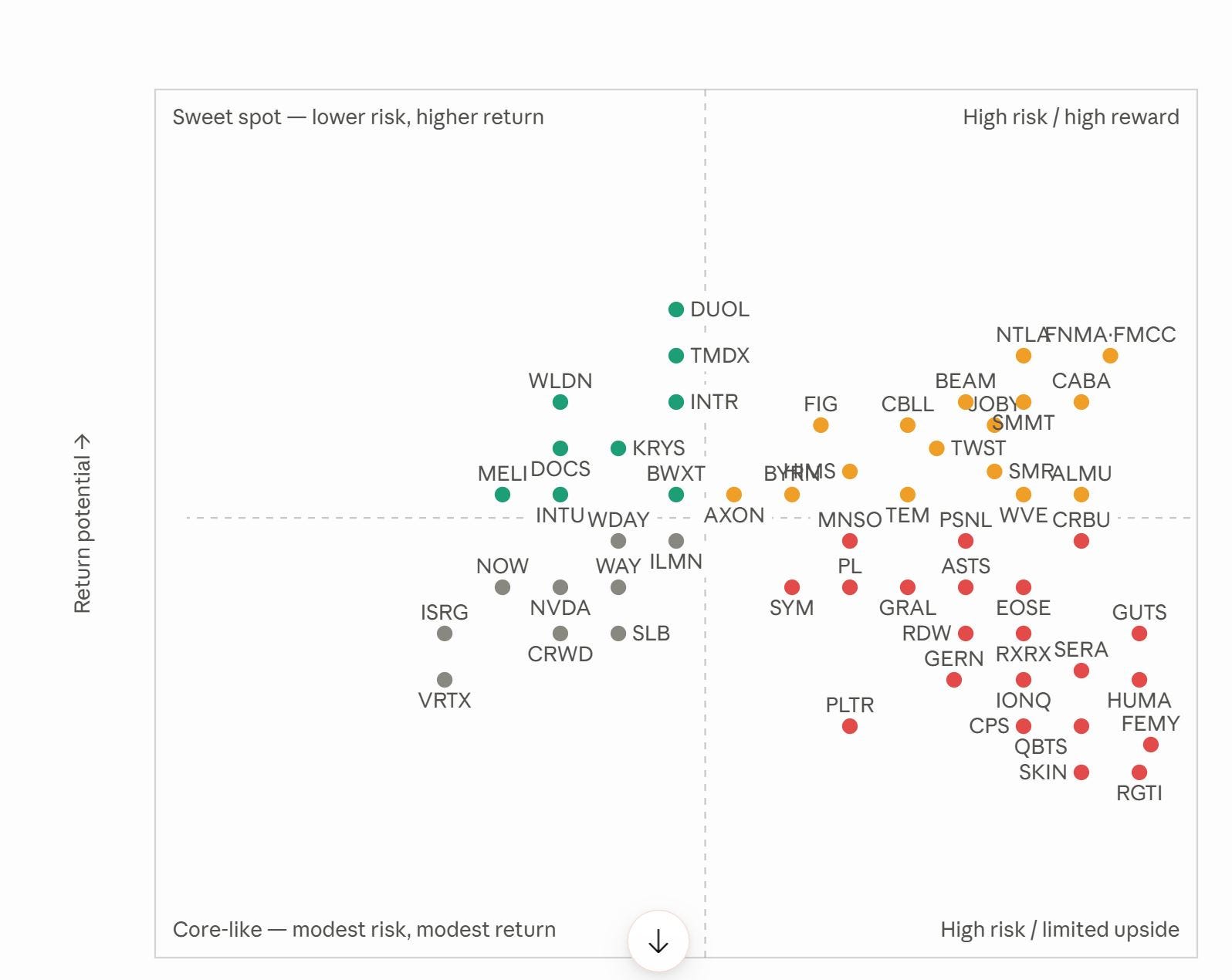

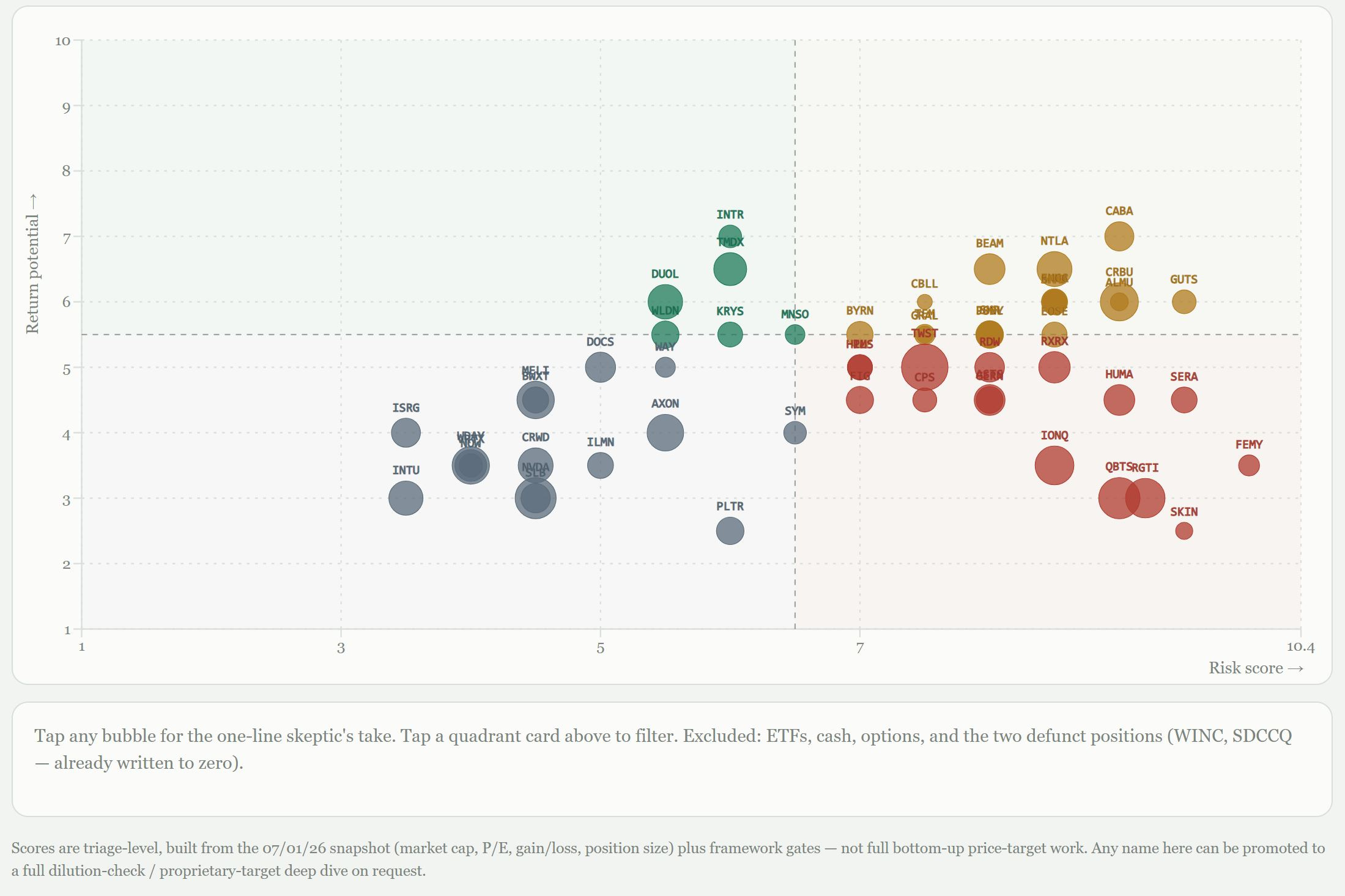

Plotting the portfolio by risk and return

Then I asked it to plot every position on a grid, risk on one axis, return potential on the other. I ran the same prompt twice in separate windows to see whether the map stayed the same.

I got a different map each time, but much of the map held. My large-cap software names sat in the low-risk, modest-return corner both times. The profitless quantum-computing and gene-editing names came back high-risk on both passes. The green cluster Fable read as limited downside with real upside didn’t move. Where the two maps split was a dozen or so names sitting right on a dividing line. CRBU and GUTS dropped out of the high-reward quadrant into the limited-upside one on the second run. FIG went the other way. AXON and PLTR crossed the risk line. MNSO, which sits near both lines at once, showed up in the sweet spot on one map and the danger zone on the other.

These models are non-deterministic. This means that the same prompt generates scores from scratch each time, resulting in slight differences. If Fable scores one ticker 5.6 on return one run and 5.4 the next, it falls on opposite sides of a line drawn at 5.5. It lands in a different quadrant even though the underlying read barely changes. That wobble is a list of the calls that are close, and those are the only ones worth your time. Fable can place the obvious names on its own. The ones that jump between runs are where the market hasn’t settled either, and where your own work has to happen.

Everything on these maps is a real position in my brokerage account. I’m showing you my book to make a point about the exercise, not handing you a buy list. What lands in my sweet spot could be wrong for yours.

High risk does not equal high return

Alarmingly, the analysis showed that 40% of my capital is in the high risk, low return area. This is an error that’s easy to make: taking on risk with the expectation of higher returns. Many people mistakenly assume risk and return are on the same dial.

Risk and return are on separate axes. High risk widens the range of possible outcomes. However, it does not say whether the top of that range is any good. A pre-revenue biotech burning cash against three competitors with a dilution problem on top is about as risky as a position gets. Its realistic upside can still be mediocre once you count the ways value leaks out before you ever see a dollar of it.

If you want to try this

Fable scores these names off what’s already been written about them, so the map it draws is the market’s current read on my portfolio and little else. I made that case in AI Will Make You a Better Investor, Not a Great One: the model gives back the consensus, and a consensus that’s already in the price isn’t an edge. A grid like this is good for seeing how my money lines up against what everyone believes and no help in finding the spot where everyone’s wrong. That part’s still mine, which is why I stay suspicious when the model likes everything I own.

What to Read Next

📖 Margin of Safety by Seth Klarman. Klarman’s framework rests on distinguishing what protects you from what only sounds like protection, which is what this quiz noticed about my portfolio’s bond allocation.

📖 Co-Intelligence by Ethan Mollick. Mollick’s argument that AI is strong in some places and weak right next to them is why I asked Fable to grade my behavior before it graded my holdings.

📖 The Dhandho Investor by Mohnish Pabrai. Pabrai’s case for a handful of properly sized bets over a pile of small ones is the fix for the two dozen souvenir positions this exercise surfaced.

🎧 All three are excellent on Audible. The free trial gives you one credit to start.

As an Amazon Associate, I earn from qualifying purchases.